Medicare Supplements

What Is a Medicare Supplement?

Medicare Supplement plans—also called Medigap policies—are offered by private insurance companies to help pay for the out-of-pocket costs that Original Medicare doesn’t cover.

When you have a Medigap policy, Medicare pays its share of your approved medical expenses first. Then, your Supplement plan helps cover the remaining costs—depending on which plan you choose, it may cover most or all of what Medicare doesn’t.

What Do Medicare Supplements Help Cover?

Original Medicare only pays about 80% of your Part B medical costs. That remaining 20% is your responsibility—unless you have a Medicare Supplement plan.

For example, if you ever require extended hospital stays or high-cost outpatient treatments, that 20% can quickly become expensive. Medicare Supplement plans are designed to help cover those extra costs and ease your financial burden.

What Don’t Medicare Supplements Cover?

Part B provides coverage for outpatient care—such as doctor visits, lab work, surgeries, specialist care, and preventive services.

There is a monthly premium for Part B. If you are receiving Social Security benefits, this premium is typically deducted from your check. If not, you’ll need to pay the premium quarterly.

Part B also has a yearly deductible. After meeting it, Medicare usually pays 80% of covered services, and you’re responsible for the remaining 20%.

Is there anything not covered by Medicare Supplement Plans?

Medicare Supplement plans only help with costs that Original Medicare covers. They do not cover things like:

Routine dental, vision, or hearing exams

Hearing aids

Eyeglasses or contact lenses

Long-term care or custodial care

Retail prescription drugs

If you need coverage for prescriptions, you’ll need a separate Part D drug plan.

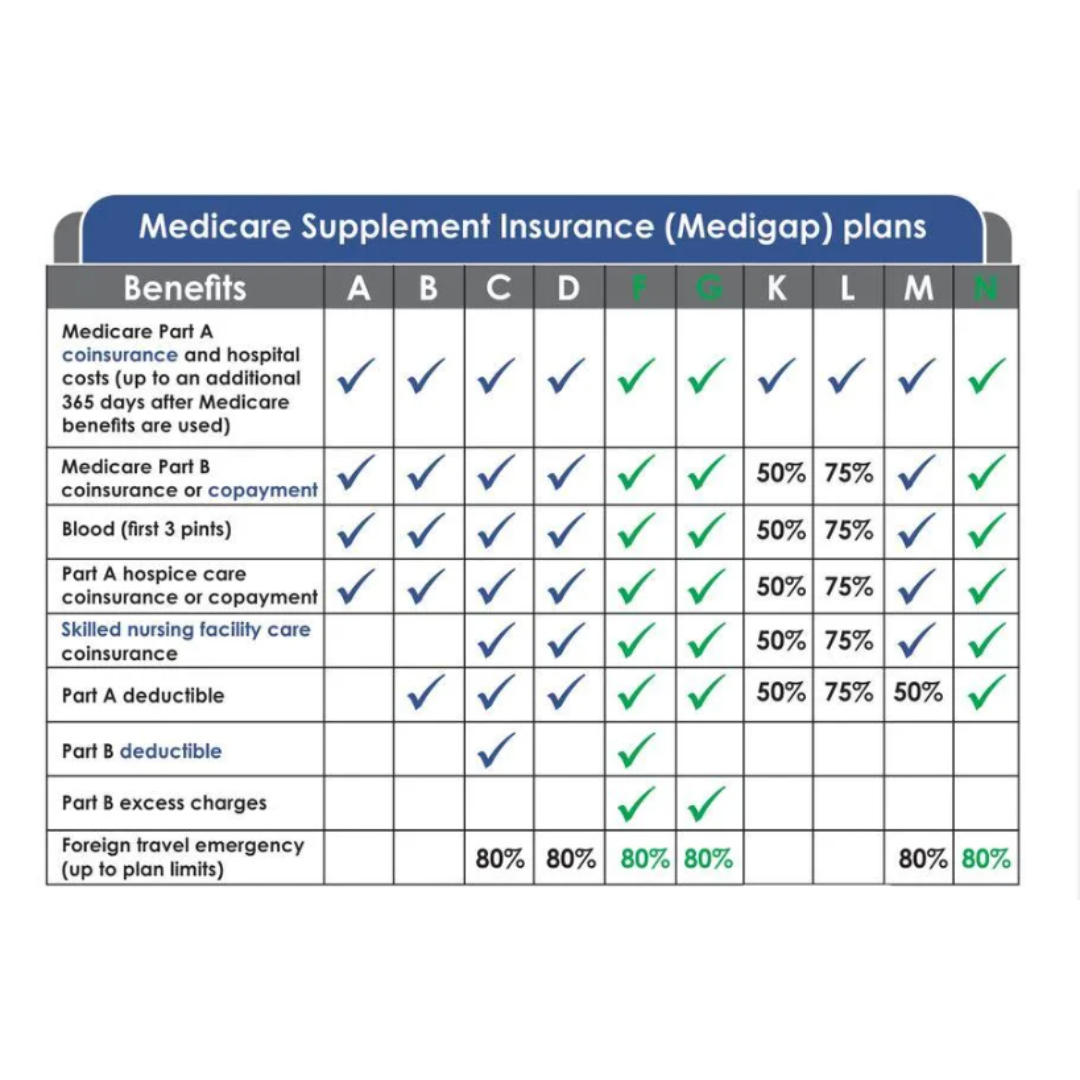

Which Medigap Plans Can I Choose From?

Plans that are highlighted in green above are the 3 most popular plans that clients choose when selecting a Medigap/Medicare Supplement plan.

Medicare Supplement Plan F

Medigap Plan F features the most coverage available of the offered Medicare Supplements.

Plan F covers the following at 100% with the exception of the foreign travel emergency benefit:

Original Medicare Part A’s deductible

Part B deductible

Part B excess charges

Part A coinsurance and hospital costs up to an additional 365 days after Medicare’s benefits are all used up

Part B coinsurance or copayments

First three pints of blood used in an approved medical procedure

Skilled nursing facility coinsurance

80% of a foreign travel emergency (up to plan limits)

Because of how much Plan F covers, it has become the most popular plan with close to 50% of clients choosing Plan F for their supplement coverage.

Currently, the only Medicare clients that still have an option to choose Plan F are those who were eligible for Medicare prior to January 1, 2020.

Medicare Supplement Plan G

Medigap Plan G features the most bang for your buck. The plan is just like a Plan F except that Plan G doesn't pay for your Part B deductible.

Plan G covers the following at 100% after you meet the Once a year Part B Deductible with the exception of the foreign travel emergency benefit:

Original Medicare Part A’s deductible

Part B excess charges

Part A coinsurance and hospital costs up to an additional 365 days after Medicare’s benefits are all used up

Part B coinsurance or copayments

First three pints of blood used in an approved medical procedure

Skilled nursing facility coinsurance

80% of a foreign travel emergency (up to plan limits)

Plan G is quickly becoming one of the most popular plans available and historically has experienced lower rate increases than it's famous brother - the Plan F.

Medicare Supplement Plan N

Medigap Plan N is one of the supplement plans that you will find with the lowest premiums due to the increase in cost share between the plan and the client. Below is what would be covered 100%:

Original Medicare Part A’s deductible

Part A coinsurance and hospital costs up to an additional 365 days after Medicare’s benefits are all used up

Part B coinsurance (AFTER a $20 office visit copay)

First three pints of blood used in an approved medical procedure

Skilled nursing facility coinsurance

Here is what you would be responsible for if you chose a Medigap Plan N:

Part B Deductible (Once a year)

$20 Office Copay

$50 Emergency Room Copay (unless checked in as an Inpatient at which point the $50 is waived)

Part B Excess Coverage

Plan N is quickly becoming one of the most popular plans available and historically has experienced lower rate increases than the Plan F or Plan G.

Office: 3333 Warrenville Rd Ste 200 Lisle, IL 50532

Call 855-223-2189

Email: [email protected]

Site: www.thefortislife.com